78% of RBF & factoring firms waste CAC, attracting businesses that don’t qualify or don’t convert.

73% of businesses applying for RBF or factoring never get approved, not due to pricing, but because of broken acquisition funnels.

61% of funded deals stall out before generating real revenue, killing long-term profitability.

A proven GTM roadmap to increasing funded applications & eliminating underwriting roadblocks.

A data-backed strategy to reduce CAC while scaling high-intent applicants.

No fluff, just actionable insights to 2X your approval rates & 3X repayment volume.

Chasing every business that applies, flooding underwriting with unqualified leads.

Relying solely on outbound & paid ads, burning CAC on low-intent clicks.

Pitching RBF as a “cheaper” alternative, without addressing borrower trust concerns.

Filtering applicants pre-click & pre-qualification, ensuring every sales conversation is worth pursuing.

Eliminating funding funnel friction, making the application & approval process seamless.

Positioning RBF & factoring as growth enablers, not just financing tools.

78% of their marketing budget was wasted on unqualified leads.

73% of applications never made it past underwriting, clogging the funnel with unviable deals.

61% of funded businesses stalled before generating real revenue, killing long-term profitability.

Google Ads for RBF cost up to $45 per click, but 60% of clicks came from pre-revenue startups that didn’t qualify.

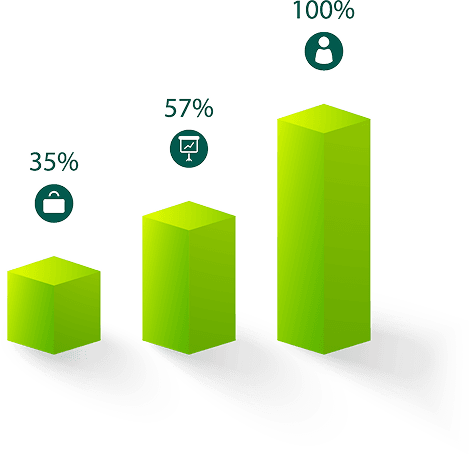

Funded applications tripled, by filtering out unqualified leads before they entered the pipeline.

Approval rates doubled, by fixing underwriting mismatches upfront.

Repayment volume increased 3X, by attracting businesses that would scale transaction volume.

CAC reduced by 50%, by eliminating ad spend waste on low-intent borrowers.

If your funding pipeline looks strong but approval rates are low, this is likely happening to you.

The firms solving this today are scaling revenue-based financing profitably, while competitors keep struggling with abandoned applications and unqualified deal flow.